How to File a Water Damage Insurance Claim in South Carolina

Filing a water damage insurance claim in South Carolina is not complicated — but homeowners who don’t understand the process consistently get worse outcomes than those who do. Knowing what to document, when to call your insurer, and how to work effectively with your adjuster can mean the difference between a fully covered restoration and a dispute that leaves you paying out of pocket for damage your policy should cover.

In this post, we cover what South Carolina homeowners insurance covers for water damage, what it doesn’t, the step-by-step claims process, and how to work with your insurance adjuster for the best outcome after a water damage event in Anderson or anywhere in Anderson County.

Water Damage in Anderson? We Work With All Insurance Carriers

Anderson Water Damage Pros handles documentation and adjuster communication directly — relieving the claims burden from you. Call (877) 698-1311.

What South Carolina Homeowners Insurance Covers

Standard homeowners insurance in South Carolina — and in Anderson County specifically — covers water damage that is sudden and accidental. The most common covered scenarios include:

- Burst or ruptured pipes: A pipe that fails suddenly and unexpectedly is typically covered. A pipe that has been leaking slowly for months and was known to the homeowner is not.

- Appliance failures: Washing machine hose ruptures, water heater failures, and dishwasher leaks that occur suddenly and without prior indication of a problem.

- Roof leaks caused by covered storms: Water that enters through a storm-damaged roof is covered if the storm itself is a covered peril (wind, hail, lightning). Roof leaks from gradual deterioration or lack of maintenance are not.

- HVAC condensate overflow: AC drain line clogs that cause ceiling leaks are typically covered as sudden and accidental events.

What South Carolina Homeowners Insurance Does NOT Cover

- Flooding from rising water: Surface water, Lake Hartwell overflow, storm surge, and any water that enters from the ground up requires separate flood insurance (NFIP or private). This is the most common misconception among Anderson County homeowners.

- Sewer backup: Not covered under standard policies unless you specifically purchased a sewer backup rider. Review your policy — this is a common gap for Anderson homeowners.

- Gradual leaks: Any water damage that resulted from a slow leak over time that the homeowner could have detected and repaired.

- Mold from neglect: Mold that developed because a known water problem was not addressed.

- Ground seepage: Water that seeps into a crawl space from surrounding soil — even if it’s from Anderson County’s clay soils — is generally not covered.

Step-by-Step SC Water Damage Insurance Claims Process

Step 1 — Stop the source immediately. Shut off your main water supply if the source is a plumbing failure. Your insurer will ask what steps you took to mitigate further damage — taking prompt action demonstrates responsible homeownership and strengthens your claim.

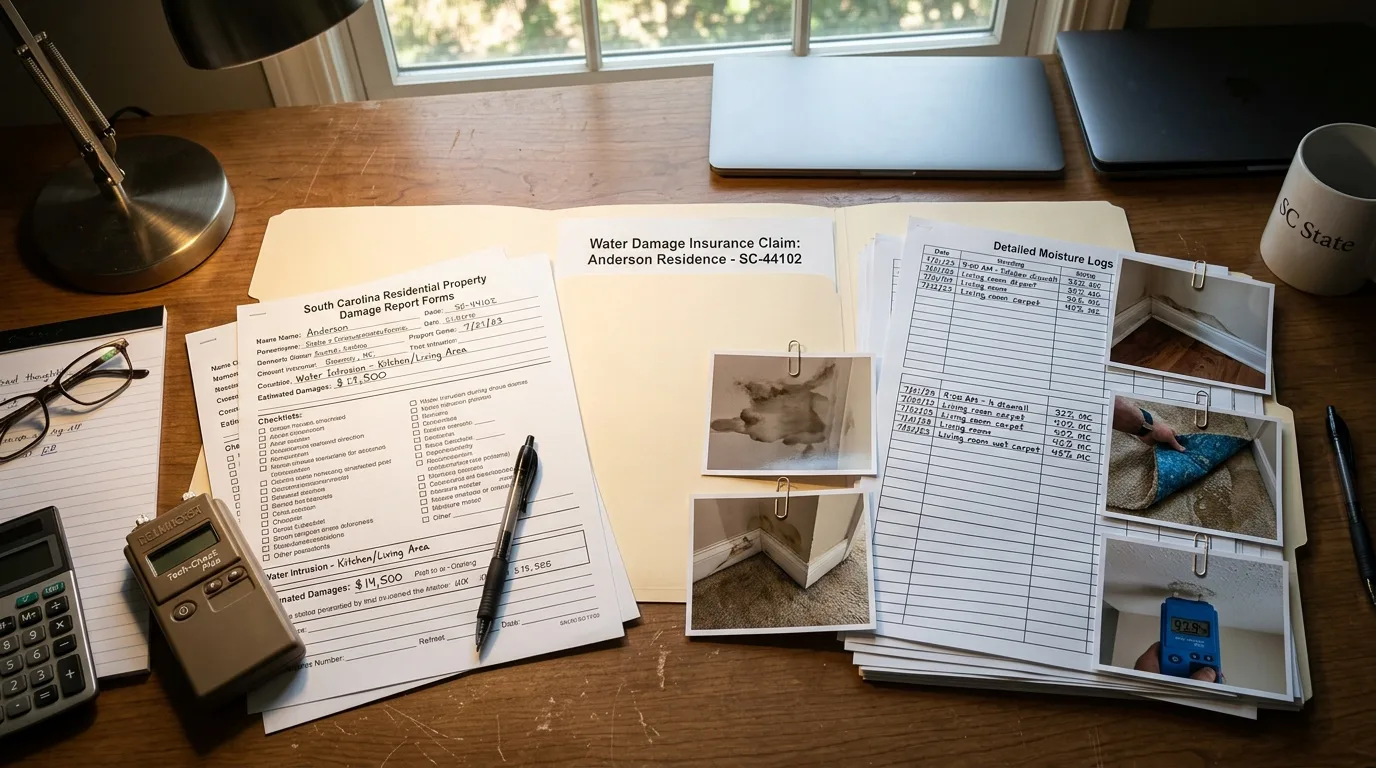

Step 2 — Document everything before any cleanup. This is the most critical step. Take photographs and video of all standing water, visible damage, the source of the water intrusion, and any affected materials — flooring, walls, ceilings, furniture, electronics. Date-stamp your photos if possible. Most smartphones do this automatically. Your adjuster needs this evidence to process the claim accurately.

Step 3 — Call your insurance company promptly. South Carolina homeowners insurance policies typically require you to report covered losses promptly — usually within 24–72 hours. Delays can be used to argue that additional damage that occurred while you waited was from neglect rather than the original covered event. File your claim as soon as the source is controlled and you have your documentation.

Step 4 — Call Anderson Water Damage Pros. Contact us at (877) 698-1311 for emergency water extraction before the adjuster visits if possible — stopping active water damage from progressing is your responsibility under your policy. We document our work thoroughly for your insurance file and communicate directly with adjusters on your behalf.

Step 5 — Work with the insurance adjuster. Your insurer will send an adjuster — either an in-house employee or an independent adjuster — to inspect the damage. Walk them through everything you documented. Be specific about what you know about the cause. If you’re uncertain about anything, say so rather than speculating. Provide the adjuster with our documentation from the extraction and initial assessment.

Step 6 — Review your settlement carefully. After the adjuster’s inspection, your insurer will provide a scope of loss estimate. Review this against our restoration estimate. If there’s a significant discrepancy, you have the right to request a re-inspection or hire a public adjuster. We can help identify items that may have been overlooked in the initial scope.

We Handle Insurance Documentation for Anderson Homeowners

Our team documents every step of the restoration for your insurance claim — and communicates directly with your adjuster. Call (877) 698-1311.

Tips for Maximizing Your Water Damage Claim in SC

Keep a home inventory. For contents claims, an itemized home inventory with approximate values is far more effective than trying to reconstruct a list of damaged items from memory after a water event. Store a copy of your inventory off-site or in cloud storage.

Save receipts for emergency mitigation costs. If you purchase wet-vac equipment, fans, or other materials in the immediate hours after a water event before our team arrives, keep all receipts — these emergency costs are typically reimbursable under your policy.

Don’t agree to “actual cash value” without reviewing replacement cost. Some SC policies pay actual cash value (depreciated value) for damaged materials, while others pay replacement cost value. Understand which your policy provides — the difference on a flooring replacement, for example, can be thousands of dollars.

Document the cause clearly. Your adjuster needs to determine whether the damage was from a covered sudden/accidental event or an uncovered gradual leak. Any evidence you have about the sequence of events — when you noticed the water, what you saw, whether there was any prior indication of a problem — strengthens your claim documentation.

Frequently Asked Questions

How long does an insurance company have to respond to a water damage claim in South Carolina?

South Carolina law (SC Code 38-59-20) requires insurance companies to acknowledge receipt of a claim within 10 business days and to accept or deny a claim within 45 days of receiving proof of loss documentation. If your insurer is not responding within these timelines, you can file a complaint with the South Carolina Department of Insurance. Most Anderson homeowners find that providing comprehensive documentation upfront significantly accelerates the claims process.

Can my insurer deny my claim if I started cleanup before the adjuster visited?

Emergency mitigation — stopping water from continuing to spread — is your responsibility under your policy and will not cause a denial if done properly. Do not permanently repair or replace damaged materials before the adjuster has inspected them unless you have explicit authorization from your insurer. Document all emergency mitigation work with photos and a professional restoration company’s written scope of work.

What if I disagree with my insurance company’s settlement offer?

Most South Carolina homeowners insurance policies include an appraisal clause that provides a dispute resolution process: you hire an appraiser, the insurer hires an appraiser, and those two appraisers select an umpire. The umpire’s decision on disputed amounts is binding. You may also hire a licensed South Carolina public adjuster who works on your behalf (typically for 10–15% of the claim payout) to negotiate with your insurer. Our restoration documentation provides the objective evidence that supports an accurate claim regardless of how any dispute is resolved.

Related:

- Water damage restoration in Anderson, SC: complete guide

- 5 signs of hidden water damage in Anderson homes

- Spring storm preparedness for Anderson SC homeowners

Insurance-Assisted Water Damage Restoration in Anderson

We work directly with all major carriers, handle adjuster communication, and provide complete claim documentation. Call Anderson Water Damage Pros at (877) 698-1311.